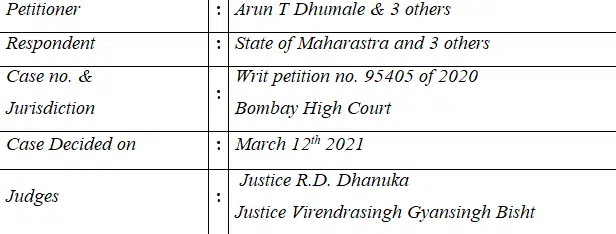

Arun T. Dhumale and 3 Ors v. State Of Maharashtra And 3 Ors

Primary Details of the case:

Arun T. Dhumale and 3 Ors v. the State Of Maharashtra And 3 Ors

Introduction

The role of cooperative banks and the regulation for them have been critically done by the banking regulations act of 1949. Why? The Reserve Bank of India is the only regulator for banks in India, so when we discuss whether RBI’s power to direct closure or open any co-operative bank under the banking regulations act of 1949 was answered by Bombay High court recently in this article it is important. It will still be a binding precedent even though it forms part of the high court until such time as a higher court overrules it should its reasoning be found incorrect. The facts and issues are as follows.

Facts

The facts surrounding this case were that the petitioners are shareholders, depositors, and other persons who had put their money into respondent CKP bank. The respondent bank was a registered cooperative society under the Maharashtra Co-operative societies act. In 1986, license was issued to this bank by Reserve Bank of India. The issue took place during 2009 where RBI sent this bank letter during its inspection mentioning that no ATMs, or counters will be operated by them apart from not opening new branches. Other restrictions were imposed on RBI in year 2012 such as reduction of borrowers to 50% and fixing accountability in the portfolio of these banks towards those borrowers. However, failure would result in liability on behalf of the bank if any non-compliance with the mechanism given to it by RBI happens according to it overview from January –June 2015.It authored directions of revival before losing cash flows along with other essential funds which had been raised and forwarded show cause notice for framing revival plan in year 2015.In later stage,new board extended time limit for preparation revival plan by two years but after submission earlier submitted revival plan turned out failure again worsening upto extension given till twenty twenty.In view thereof ,on April twenty eighth two thousand twenty nineteen,RBI revoked licence granted to said bank as there was failure in compliance with statutory provision provided under section 22 of the banking regulations act, 1949. Petitioners have challenged this order in the present case on ground which we are going to consider and also sought a prerogative writ for an order of mandamus directed at RBI.

Issues

Meanwhile, the following questions were answered by Bombay High Court:

Could such action be justified with reference to either the role of Reserve Bank of India under section 22 read with section 56 of Banking Regulations Act, 1949 or not? If so indicate my dear friend what are those reasons behind it?

Secondly, does this actions against principles of natural justice and rule of law as contended by petitioners?

Laws involved

Section 22 read with section 56of Banking Regulations act,1949

Cooperative Societies under the act should comply with directives of RBI (Section110 (A) (1) (iii) of Maharashtra Co-operative Societies Act).

Contentions

The respondents claimed that the Reserve Bank of India (RBI) was in breach of principles of natural justice and due process of law when it ordered cancellation of the CKP bank license, among others.

They pointed out that between 2015 and 2020 a delay by around five years in issuing the show cause notice. Therefore, on these grounds the petitioners prayed for nullification by a court of law for the impugned orders made by the Reserve Bank of India.

According to RBI’s submissions, there was enough time given to CKP bank concerned and even after those directions towards compliance were under section 22, its compliance was not failed to be complied with. This means that cancellation is only valid to protect depositors and members of the bank or up to such an extent.

Verdict:

Upon examining this matter, a High Court bench observed as follows:

Reserve bank does not have simply to act as watchdog on each aspect about banks licensed to carry out banking business. Not every internal matter need be looked into but areas statutorily required o be scrutinized will have mandatory supervision. The reserve bank shall look into non-compliance with conditions for granting banking licenses from time-to-time.

It also considered another role of RBI which said that if the relevant bank has failed several times in following its directions then it should be cancelled through its order even though there may still be public interest involved here i.e., for the sake of depositors and other stakeholders at large who are mainly members/beneficiaries of that particular institution.

The court noted how no revival could take place at that instant when a decision was made to cancel thereto. In case Reserve Bank thinks such would prejudice holders or members interests thereby will not give any opportunity on this occasion according any right or title thereof.

For this case, it held that despite having many chances where CKP Bank has been requested either to merge itself with any financial stable banks it has totally failed to do so and hence did not comply with the directives under section 22 of the Banking Regulations act of 1949. Consequently, it found that RBI was justified in making decision to cancel license of the respondent bank and its move was based on its statutory power provided for in section 22(4) of the Banking Regulations act.

Conclusion:

From the above case, two key observations can be made. One is that RBI has power to give directions to cooperative banks under the Maharashtra Co-operative Societies Act. Second, if the bank’s action is found by RBI to be against public interest and depositors’ interests, its license can be revoked in terms of section 22 (4) of Banking Regulations Act 1949 as RBI is a watchdog for the protection of Depositors, Public and Banking Business in India. Notably article 19(1) (g) fundamental right stands nowhere compared to power of RBI under section 22. It is with respect to this stand of judiciary on power given to RBI by section 22 that we think should be followed unless it becomes unfair and irrational.